New money market charts and series published

23 April 2026

By Ronald Rühmkorf and Martina Vesan

On 22 April 2026 the ECB released a set of new data for the first time: the Extended Money Market Statistics, which provide additional insights into the euro money market. The new money market data series are being made available following frequent requests from data users. These data series were used to generate the charts in Part II of the Euro Money Market Study 2024 and have now been integrated into a new money market dashboard in the ECB Data Portal. The new series and charts focus on money market indicators that are particularly relevant for understanding market dynamics, e.g. for exploring the spread between one-day rates and the deposit facility rate (DFR), the transmission of ECB rate changes to money market rates, or quarter-end and year-end effects on borrowing and lending volumes and rates.

The Extended Money Market Statistics cover the five key segments of the euro money market: (i) secured transactions – repurchase agreements (repos) and reverse repos, (ii) unsecured cash transactions, (iii) short-term securities issuance (STS), (iv) foreign exchange swaps, and (v) overnight index swaps. The new dashboard makes it possible to explore the developments in these money market segments, showing various dimensions of the market such as volumes, prices, counterparties, maturities and calendar effects.

Most of the new series are based on data collected under the Money Market Statistical Reporting (MMSR) Regulation.[1] They are complemented by data from the Centralised Securities Database (CSDB), the Securities Holdings Statistics (SHS) and the European Market Infrastructure Regulation (EMIR).[2] The published time series generally cover the time period from the beginning of 2017 until the end of 2025. The new series will be updated annually.

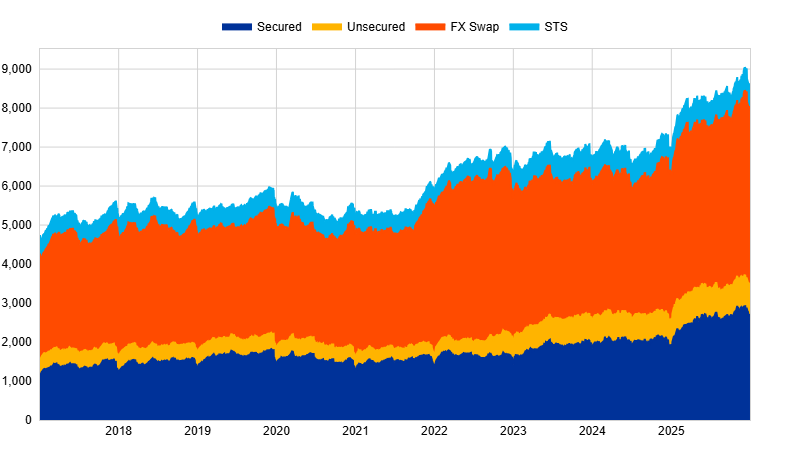

In comparison to the MMSR data series already being published, the new series cover additional breakdowns, frequencies and concepts, e.g. they include a new series on outstanding amounts per market segment (Chart 1).

Chart 1

Outstanding amounts by money market segment

Outstanding amounts have continued to grow from €7 trillion in 2024 to €8.5 trillion at the end of 2025, representing an increase of about 23%. While secured transactions dominate the money market in terms of daily turnover (Chart 2), FX swaps account for the largest share of outstanding amounts owing to their typically much longer maturities.

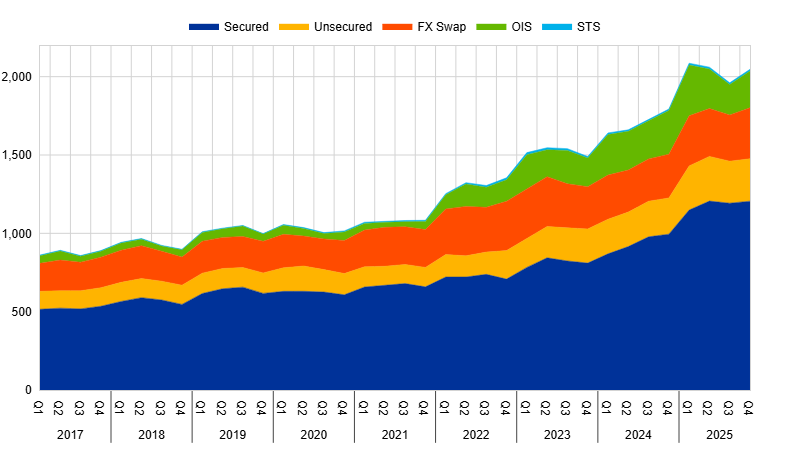

Growth in daily turnover in 2025 was about 20%, roughly in line with growth in outstanding amounts. The increase was concentrated in secured and unsecured transactions with very short maturities. By contrast, the daily turnover in the OIS segment declined in the second half of 2025, with a reduction of forward transactions following lower market uncertainty around future policy rates.

Chart 2

Daily average volume per segment

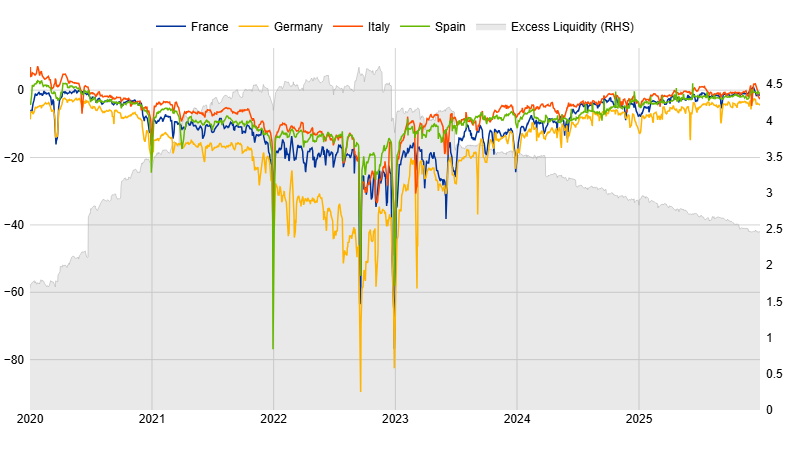

Regarding developments in money market rates, in 2025 one-day repo rates continued to converge with the DFR as collateral scarcity continued to ease (Chart 3). In comparison to previous years, the scarcity premium for transactions involving high-quality collateral decreased. One-day unsecured rates also continued to converge with the DFR, while the positive spread of secured rates over unsecured rates remained. For a recent discussion on money market rates see also the post in The ECB Blog on “How banks adjust to declining reserves”.

Chart 3

One-day repo rate vs DFR

Further information

Extended Money Market Statistics dataset

[1] Regulation (EU) No 1333/2014 of the European Central Bank of 26 November 2014 concerning statistics on the money markets (ECB/2014/48) (OJ L 359, 16.12.2014, p. 97).

[2] Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories (OJ L 201, 27.7.2012, p. 1).